Table of Contents

Introduction: A Quiet Sunday, a Giant Step

Early on April 20, 2026, while most Americans were still relaxing into their morning routine, a deal fell through that barely made a splash in financial circles – but it should have.

QXO announced that it will acquire Topbuild Corp for $17 billion.

No attractive consumer brand. No viral headlines. No AI hype.

Just insulation, roofing systems, waterproofing – and one of the most aggressive industrial consolidation plays in decades.

At the center of it all is Brad Jacobs, a man who has built – and scaled – multibillion-dollar companies by doing one thing better than almost anyone else: buying fragmented industries and turning them into machines.

This is not just another acquisition. It’s part of a $30 billion blitz over 13 months that is reshaping how America builds homes, warehouses, factories and data centers.

Let’s break it down properly – no fluff, no hype – just what’s really happening, why it matters, and where this is going next.

1. The Deal, Explained: What QXO Is Really Buying

Topbuild Isn’t Sexy – But It’s Extremely Valuable

Topbuild Doesn’t Sell to Customers. You won’t see it on a billboard.

What it does is more important:

- Installs insulation (spray foam, fiberglass, blow-in)

- Distributes building materials nationwide

- Serves residential, commercial, and industrial construction

It operates through two main divisions:

- TruTeam → Installation Services

- Service Partners → Distribution Network

Most companies do one or the other. Topbuild does both – and that’s where the edge comes from.

Why Topbuild Was Valued at $17 Billion

Let’s get this down to the basics:

- Adjusted EBITDA margin: ~18% (elite for this industry)

- National footprint

- Deep contractor relationships

- Operational discipline (rare at scale)

That 18% margin is important. In construction distribution, where margins are typically thin, it signals tight execution, pricing power, and efficiency.

Jacobs isn’t just buying income. They are buying a system that already works better than most competitors.

Deal Structure (And Why It Matters)

Price: $505 per share

Premium: ~23%

Structure:

- 45% cash

- 55% stock

Topbuild shareholders can choose to:

- Take guaranteed cash

- Or take QXO stock (20.2 shares equivalent)

This is where the real decision lies.

Cash = certainty

Stock = bet on Jacobs

Given QXO’s ~90% stock growth over the past year, this is not trivial. You are either withholding benefits or doubling down on the rollup strategy.

2. QXO Rollup Strategy: This Is Not Your Typical Private Equity Play

Let’s be clear: most rollups are typical.

They buy smaller companies, cut costs and hope that margins will improve.

Jacobs doesn’t do that.

Jacobs’ Playbook (Simple)

- Find a fragmented industry

- Employ aggressive capital quickly

- Acquire category leaders

- Use logistics as a weapon

- Scale aggressively

He’s done it before:

- United Rentals

- XPO Logistics

- GXO

- RXO

And now he’s doing it again – with construction materials.

Why Fragmentation = Opportunity

The U.S. building products market is huge:

- $300+ billion addressable market

- Thousands of regional players

- No dominant national operator

It creates inefficiencies:

- Different pricing across regions

- Inconsistent delivery speeds

- Fragmented supplier relationships

Jacobs sees it and thinks one thing:

“This could be centralized – and monetized.”

QXO Purchase Momentum Timeline

March 2025:

$11 billion acquisition of Beacon Roofing Supply

February 2026:

$2.25 billion acquisition of Kodiak Building Partners

April 2026:

$17 billion acquisition of Topbuild

Three major deals. Thirteen months.

It’s not aggressive – it’s borderline reckless unless the implementation is elite.

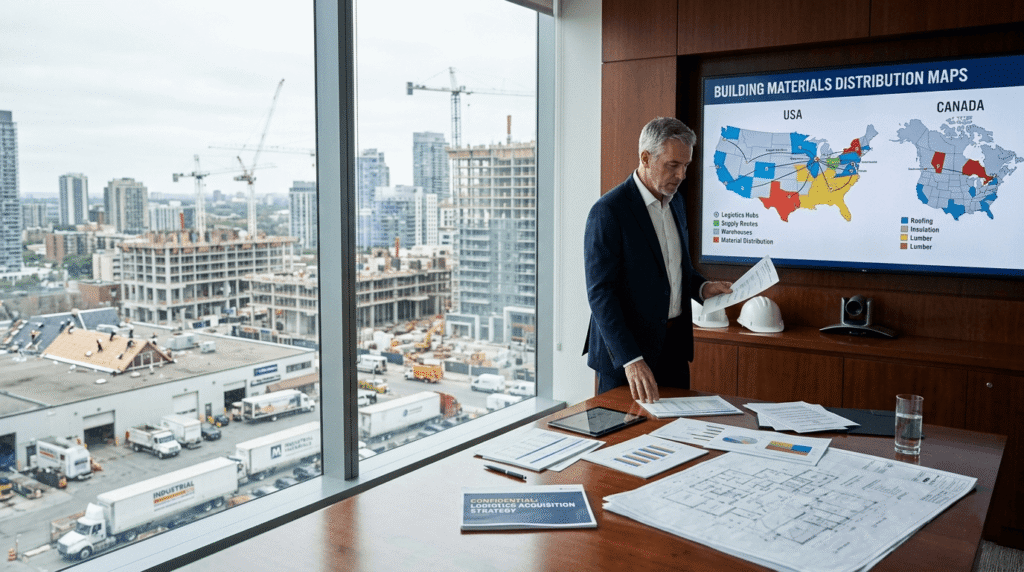

The Real Edge: Logistics

This is where most people underestimate strategy.

A company with:

- 1,150 locations

- 10,000+ vehicles

- National routing systems

…can deliver faster, cheaper, and more reliably than regional competitors.

In construction, it is more important than branding.

Contractors don’t care about your logo.

They care whether the content appears on time or not.

3. Hidden Corner: Data Centers (This is Bigger Than Housing)

The deal announcement had one key phrase pressed:

Expansion into large-scale projects like data centers

That’s not a side note. That’s the real story.

Why Data Centers Matter

Companies like:

- Microsoft

- Amazon

- Meta

…are spending hundreds of billions to build infrastructure for AI.

Data centers need:

- Advanced insulation

- Moisture control

- Thermal efficiency

Topbuild works exactly where it counts.

Translation

This is not just a housing drama.

It’s a picks-and-shovels strategy for the AI boom.

While everyone else is buying AI stocks, Jacobs is selling the stuff that builds the physical infrastructure behind them.

It is a more sustainable position.

4. The Numbers Behind The Deal

Let’s cut through the headlines and look at the actual valuation.

Key Metrics

- Deal Value: $17 Billion

- EV/EBITDA (Pre-Synergy): ~14.9x

- EV/EBITDA (Post-Synergy): ~11.8x

- Expected Synergy: $300 Million Annually by 2030

Snapshot of The Combined Company

Post-Acquisition:

- Revenue: $18 Billion+

- EBITDA: $2 Billion+

- Employees: 28,000

- Locations: 1,150

Competitive Benchmarks

Ferguson Enterprises Remains an Industry Leader:

- Market Cap: ~$50 Billion

QXO:

- Market Cap: ~$17–18 Billion

Gap (and Betting)

If Jacobs Executes:

- That Valuation Gap Narrows

- QXO Rebounds

- Equity Holders Win Big

If It Doesn’t Does:

- Integration fails

- Synergies are missed

- Shares get punished

There is no middle ground here.

5. Brad Jacobs Blueprint: How He Builds Empires

Let’s break this down into principles, not personalities.

1. Target “Boring” Industries

Avoid those hyped areas.

Why?

Because boring industries:

- Are fragmented

- Lack efficiency

- Have price inconsistencies

That’s where integration works best.

2. Get Big Right Away

Most companies scale slowly.

Jacobs does the opposite:

- Starts with a big acquisition

- Gains instant market relevance

It’s risky – but it compresses time.

3. Logistics Is The Moat

Not branding. No product innovation.

Execution.

Fast delivery = pricing power.

4. Operators Rather Than Bankers

He doesn’t just buy companies.

It keeps strong operating teams and scales their systems.

Topbuild’s “Special OPS” culture is a great example.

5. Use Stocks as Currency

When your stock is rising, it becomes cheap acquisition capital.

QXO is doing exactly that.

6. What This Means For The U.S. Housing Market

Let’s get real: Housing is in disarray right now.

Short-Term Reality (2026)

- Mortgage rates still high

- Housing starts inconsistent

- Builder sentiment mixed

That puts near-term pressure on Topbuild’s core business.

Long-Term Reality

There is still a housing shortage in the U.S.:

- Estimate: 3.5 million–7 million units

Demand is not optional – it is delayed.

Jacobs’ Bet

He’s not betting on 2026.

He’s betting on:

- 2028

- 2030

- Beyond

If he survives the recession, he’ll dominate the recovery.

7. Competitive Landscape: Who Should Worry

Ferguson Enterprises

Still Dominant – For Now.

But QXO is:

- Faster growing

- More aggressive

- More acquisition-driven

It forces Ferguson to stay sharp.

Regional Players

This is where things get ugly.

They now face:

- National pricing pressures

- Fast delivery competitors

- Large purchasing power

Their options:

- Differentiate deeply

- Or acquire

Most cannot survive independently.

Contractors (The Wild Card)

They benefit from:

- Better pricing

- Large inventory

- Fast delivery

But risks:

- Bureaucracy

- Integration chaos

- Reduced flexibility

The implementation of QXO here will determine whether this strategy works or not.

8. Integration Risk: The Part No One Wants to Talk About

Here’s the uncomfortable truth:

This could go wrong. Fast.

Problem

Three major acquisitions in 13 months:

- Beacon → Not fully integrated

- Kodiak → Just closed

- Topbuild → Incoming

That’s a huge organizational strain.

Where Deals Fail

- Cultural clashes

- System incompatibility

- Employee resistance

- Customer disruption

Synergy doesn’t fail on spreadsheets.

They fail in warehouses and sales teams.

The Only Reason This Could Work Is

Jacobs has done it before.

Over and over again.

It doesn’t eliminate the risk – it just reduces it.

9. Macro Tailwinds: Why This Industry Really Makes Sense

This is not random timing.

There are real structural drivers here.

1. Energy Efficiency Regulations

Stricter building codes = more insulation demands.

Guaranteed growth.

2. Industrial Reshoring

Factories are coming back to the U.S.

They all need construction materials.

3. Data Center Explosion

AI infrastructure = physical buildings.

Those buildings need exactly what QXO sells.

4. Climate Resilience

Severe weather = better building standards.

More insulation, better sealing, more demand.

10. The Long Game: Where QXO Could Be by 2030

Let’s model this without the hype.

Base Case

- Revenues continue to grow

- Synergies partially realized

- EBITDA ~ $2.5B–$3B

Converse Case

- Full synergy capture

- Strong housing recovery

- Ongoing acquisitions

Outcome:

- EBITDA: $3B+

- Valuation multiple: ~15x

- Market cap: ~$45B

Reality Check

This only works if:

- Integration is successful

- Housing stabilizes

- Execution remains tight

Otherwise, this gets tricky.

11. Was $505 a Fair Price For The Topbuild?

Short answer: Yes, but context is important.

Bull Case

- 23% premium = strong exit

- Near-term housing risk exists

- Locking benefits make sense

Bear Case

- Topbuild had standalone growth

- Strong margins and positioning

- Could have compounded independently

Realistic Reality

Few companies can beat the Jacobs-led rollup on scale.

So the premium is:

Reasonable – and perhaps a little generous given current conditions.

Consolidation Intelligence Framework

Use this to properly analyze any future trade.

1. Fragmentation Check

If top players don’t dominate → Rollup opportunity.

2. Logistics Advantage

If scale improves delivery → a real pit exists.

3. Consolidation Reality

Check whether earnings growth is real or accounting-based.

4. Macro Alignment

Is the industry growing structurally or cyclically?

5. Integration Speed

Too fast = implementation risk.

6. Stocks as Currency

If stocks fall, the entire strategy is weakened.

Final Verdict: High-Commitment Bet With Real Risk

This deal makes sense.

That doesn’t mean it’s safe.

Brad Jacobs is executing a consistent, aggressive strategy in an industry that truly supports consolidation. Macro tailwinds are real. The operational logic is correct.

But the burden of implementation is very large.

Three big mergers at once are where even the strongest operators break down.

Bottom Line

- Strategically? Strong.

- Operationally? Challenging.

- Risk Level? High.

- Upside? Significant.

If this works, QXO becomes a dominant force in the $300 billion industry.

If that doesn’t happen, this becomes a case study in overextension.

Anyway, this isn’t boring anymore.

Frequently Asked Questions

What exactly does TopBuild do, and why does it matter?

Topbuild installs and distributes insulation and building materials throughout the U.S. It is deeply embedded in the construction workflow, particularly in residential and commercial projects.

What makes it valuable is not the product – it’s the network and the implementation. Contractors rely on consistent delivery and service, and Topbuild has built that on a large scale. It is difficult to repeat and even more difficult to break.

Who is Brad Jacobs, and why should you care?

Brad Jacobs is one of the most successful industrial rollup builders in modern U.S. business. He has built multi-billion dollar companies by integrating fragmented industries and scaling them efficiently.

You should be careful because their track record suggests that this is not random aggression – it is a repeated strategy. However, past success does not guarantee future results, especially at this pace and scale.

Should investors choose cash or QXO stock?

This depends on risk tolerance and time horizon. Cash is locked into a guaranteed premium – no surprises. The stock lets you experience the benefits of QXO but also the risk of its implementation.

If you think Jacobs can pull off another successful rollup, the stock could perform even better. If you’re not sure – or you don’t want the volatility – cash is the smartest move.

What are the biggest risks in this deal?

Three key issues:

1) Integration overload from multiple acquisitions

2) Slowdown in housing market impacts demand

3) Failure to realize synergies

These are not small issues – they are exactly where big deals fail.

What does this mean for the construction industry as a whole?

It accelerates consolidation. Smaller players will either become specialists or be acquired. Big players will grow faster.

The industry is shifting from fragmented and local to national and system-driven. It changes prices, competition, and customer expectations.